The digital economy is undergoing a fundamental transformation. We are moving away from an internet where humans search, compare, and click, to an ecosystem where artificial intelligence agents perform these actions on our behalf. For C-level decision makers in banking, financial services, and insurance, this shift requires a complete reevaluation of digital strategy. Agentic commerce in Banking, Financial Services and Insurance (BFSI) is no longer a future concept. It is a present reality reshaping how transactions occur, how credit is distributed, or how customer relationships are maintained.

Financial institutions that prepare their infrastructure today will capture the value of this new automated economy. Those that wait will find themselves disconnected from the customer journey. We want to help you understand exactly what agentic commerce means for your organization, how the underlying infrastructure works, and what concrete steps you must take to secure your position in this emerging landscape.

Understanding Agentic Commerce

To build a strategy for agentic commerce in banks, fintechs, financial services, and insurance, we first need to separate reality from hype. Agentic Commerce is fundamentally different from traditional e-commerce, and it goes far beyond the capabilities of basic chatbots or customer service automation.

In the traditional model of assisted commerce, digital tools help a human make a decision. A user might ask an AI assistant to find the best auto insurance rates or recommend a credit card with no foreign transaction fees. The assistant provides information, but the human user must still navigate to the provider's website, fill out the application, verify their identity, and complete the transaction.

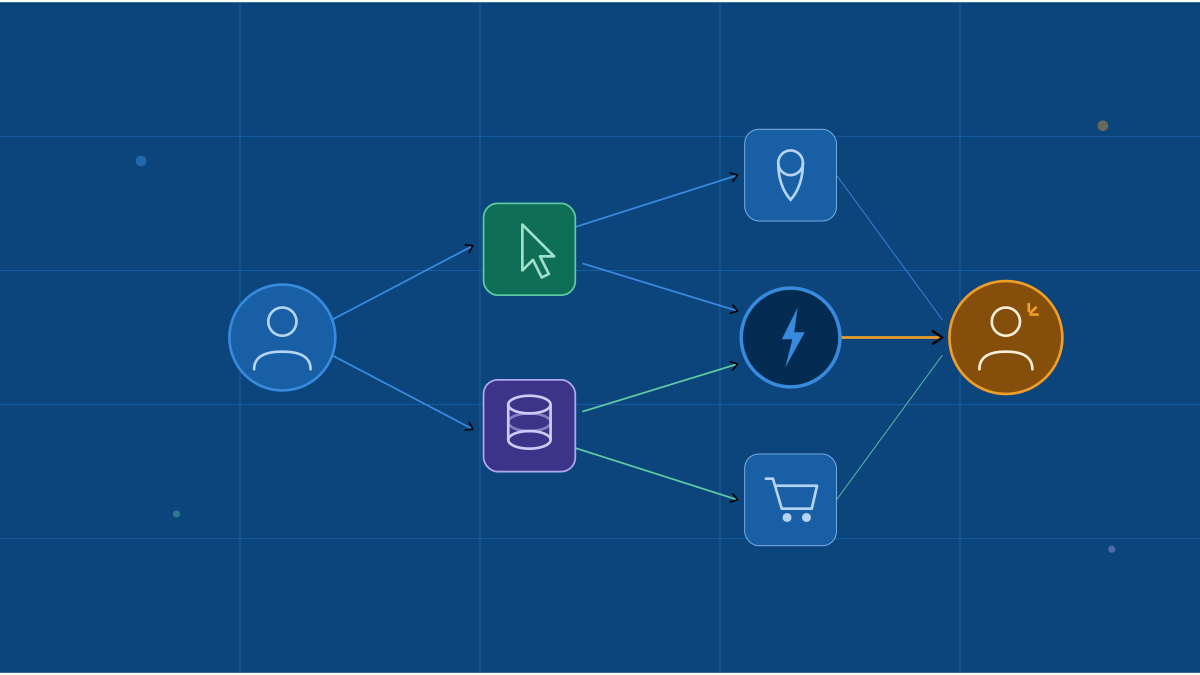

Agentic commerce removes this friction. In an agentic system, the user delegates authority to an AI agent to execute complex, multi-step tasks autonomously. The agent interprets the user's intent, scans the market, compares options based on deeply personal historical data, negotiates terms, and executes the final transaction without requiring the human to intervene. The agent does not just assist. It acts.

For the BFSI sector, this represents a structural change in how products are discovered and consumed. If an AI agent is evaluating which wealth management platform to use or which business loan offers the best terms, your marketing materials and search engine optimization strategies are no longer enough. Your products, APIs, and data structures must be entirely legible to machines. If an AI agent cannot read your product attributes, compare your rates in real time, and securely authenticate a transaction through your systems, your institution simply will not appear in the agentic checkout process.

The Scale of AI Agentic Commerce Is Already Here

If you believe this technology is still in an experimental phase, the market data tells a different story. Leading organizations are already operating agentic systems at a massive global scale, proving that consumer behavior is shifting rapidly.

Consider how Amazon has deployed its AI shopping agent, Rufus. Launched in early 2024, the agent is already active across the United States, the United Kingdom, India, France, Germany, Italy, Spain, and Canada. More than 300 million customers used Rufus during 2025. This agent goes far beyond answering basic questions. It tracks prices, makes complex product comparisons, remembers personal shopping histories, and executes autonomous purchases through a specific feature that buys items for the user.

The financial impact of this capability is extraordinary. According to Amazon's Q4 2025 results, interactions grew by 210% year over year. More importantly, users interacting with the agent showed a 60 percent higher likelihood of completing a purchase compared to non-users. This resulted in 12 billion dollars in annualized incremental sales attributed directly to the agent in 2025, easily surpassing their initial 10 billion dollar projection. On a daily basis, the system handled 274 million queries in October 2024, representing 13.7% of all searches on the platform.

For banking and insurance executives, the lesson here is profound. The behavioral expectation for AI mediated commerce is already installed in hundreds of millions of consumers. When your clients interact with your financial products, they will expect the same level of seamless, autonomous execution. They will want their personal financial agents to manage their subscriptions, optimize their savings yields, and renew their insurance policies automatically. The challenge for your institution is ensuring your infrastructure is ready to facilitate these agent driven actions.

Security, Compliance, and Identity in AI Commerce

For technology and operations leaders in banking and insurance, the shift toward agentic AI commerce introduces complex new challenges in security, risk management, and regulatory compliance. Allowing an autonomous software program to execute financial transactions fundamentally alters your threat landscape.

The primary security mechanism protecting agentic commerce is tokenization. Because the AI agent utilizes network tokens rather than primary account numbers, the risk of a massive data breach exposing sensitive financial information is heavily mitigated. Even if a malicious actor compromised an AI assistant, they would only acquire a token that is mathematically restricted to specific transaction types, merchants, and spending limits.

However, tokenization alone does not solve the identity challenge. Financial institutions must implement sophisticated authentication protocols to verify that the agent initiating a transaction is truly acting on behalf of the verified customer. This requires integrating your identity access management systems with new industry standards like the Trusted Agent Protocol. When an agent attempts to initiate a transfer or authorize a payment, your systems must be able to validate the cryptographic signature of the agent in milliseconds, checking it against the predefined parameters established by the human account holder.

Compliance teams must also adapt to this new paradigm. Anti money laundering regulations and Know Your Customer (KYC) rules were designed for human actors. When agents begin executing high frequency micro transactions or autonomously shifting funds between different wealth management products to optimize yield, traditional monitoring rules will generate an unmanageable volume of false positives.

The Checkout Implications for Financial Institutions

The rise of Agentic Commerce forces banks and credit card issuers to confront a new strategic threat. We call this the invisible funnel. As AI agents increasingly manage the discovery and selection phases of the customer journey, traditional brand loyalty diminishes.

Consider how a consumer selects a credit card or a loan today. They might visit your bank's website, see your marketing promotions, and choose your product based on brand affinity or a user friendly digital experience. In an agentic future, the consumer simply tells their AI assistant to find the lowest interest rate or the highest cash back yield. The agent bypasses your marketing entirely, evaluating your products purely on raw data and API accessibility.

If your core banking systems cannot expose product details, dynamic pricing, and underwriting criteria through secure, machine readable interfaces, the AI agent will simply ignore your institution. It will direct the customer's business to a more technologically agile competitor.

This shift also impacts the point of checkout. When a transaction is fully agentic, the traditional checkout page disappears. The agent negotiates the final price and transmits the tokenized payment credential instantly in the background. If your bank's fraud systems introduce unnecessary friction, requiring manual SMS verification for an authorized agentic transaction, the agent will likely abandon the process and use a secondary payment method from a different issuer.

To maintain top of wallet status, financial institutions must ensure their payment credentials are fully compatible with intelligent commerce platforms. You must actively participate in these new ecosystems, providing the necessary APIs so your cards and accounts can be seamlessly provisioned into the leading AI assistants.

Concrete Steps for Banks, Fintechs, and Insurers

Transitioning your organization to support Agentic Commerce requires a structured, deliberate approach. We recommend C-level leaders focus on the following concrete steps to modernize their infrastructure safely.

First, you must conduct a comprehensive audit of your API ecosystem. Agentic Commerce relies entirely on machine to machine communication. If your legacy core banking or insurance administration systems rely on screen scraping or batch processing, you cannot participate in real time agentic transactions. You need to build modern, secure, RESTful APIs that expose your product catalogs, pricing models, and transaction endpoints to authorized AI platforms.

Second, you must redefine your data architecture to ensure absolute legibility for machines. AI agents rely on massive language models to understand the world. If your product descriptions, terms of service, and fee schedules are locked in unstructured PDF documents or scattered across disconnected databases, the agents cannot evaluate them. You must structure your data comprehensively, using clear metadata and standardized financial schemas, ensuring that an agent can accurately compare your offerings against the wider market.

Third, you must implement the infrastructure to support AI ready tokenized credentials. Work closely with major networks to upgrade your card issuing platforms. Your mobile banking applications should allow customers to easily provision their accounts directly to their preferred AI assistants, giving the user clear, granular control over spending limits, geographic restrictions, and merchant categories.

Fourth, you must design intelligent exception handling workflows. Map out your most critical customer journeys and define the exact parameters where an AI agent must stop and hand the process over to a human specialist. Build the internal routing tools necessary to transfer the full context of the agent's interaction to your human employees instantly, ensuring the customer never has to repeat themselves.

Fifth, you must upgrade your real time fraud monitoring systems. You need AI driven security models capable of analyzing the velocity, context, and cryptographic signatures of agentic transactions. Establish clear rules for participating in the Trusted Agent Protocol, ensuring your systems automatically reject transactions from unverified or suspicious automated entities.

The Strategic Imperative for Leaders

Agentic commerce in BFSI is not an isolated technology trend. It represents a fundamental rewiring of how financial value is discovered, negotiated, and exchanged in the digital world. The early adopters are already operating at scale, processing millions of transactions and generating billions in incremental value through highly automated, highly efficient AI networks.

For technology, operations, and business strategy leaders, the mandate is clear. You can no longer rely on legacy customer interfaces or traditional e-commerce paradigms. You must adapt your infrastructure to receive, process, and secure transactions initiated by intelligent agents.

We understand the complexity of this transformation. Integrating legacy financial systems with cutting edge AI protocols requires deep technical expertise, stringent security controls, and a clear vision for the future of your business. By building robust APIs, structuring your data for machine legibility, embracing new tokenized payment networks, and designing thoughtful human in the loop governance, you can ensure your institution thrives in the era of agentic finance.

The infrastructure for the next generation of commerce is being built right now. The leaders who actively participate in designing this ecosystem will secure their relationships with the next generation of consumers, driving sustainable growth, operational efficiency, and unshakeable customer trust in an increasingly automated world.